Tax Planning Update: One, Big, Beautiful Bill

On July 4, 2025, President Trump signed into law the One, Big, Beautiful Bill Act (OBBBA). It includes changes and extended provisions that may have significant implications for taxpayers. We have highlighted some of the key features of the new legislation impacting income taxes, estate planning, nonprofits, and businesses. As we continue to analyze this complex new legislation, we will keep you informed with updates and planning opportunities as additional details become available.

Key Income, Estate, and Charitable Planning Features:

- Estate, Gift and GST Taxes – The bill permanently extends the estate tax provisions of the Tax Cuts and Jobs Act (TCJA) that were set to expire at the end of 2025. The exemption for estate, gift and GST taxes has been permanently increased to $15 million per person ($30 million per married couple) starting in 2026, with indexing for inflation going forward.

- State and Local Taxes (SALT) – The cap on deductions for state and local taxes (the SALT cap) will be increased from $10,000 to $40,000 starting in 2025 for taxpayers earning $500,000 ($250,000 for married filing separately) or less. Both the cap and the income threshold will increase 1% every year until reverting back to $10,000 in 2030. The increased SALT cap phases down by 30% of the excess of the taxpayers’ income over $500,000, with a floor of $10,000. Taxpayers with income of $600,000 or more will get no benefit from the One, Big, Beautiful Bill and are capped at a SALT deduction of $10,000.

- Tax Rates and Brackets – The seven income tax brackets and their corresponding rates initially enacted in the 2017 TCJA have been made permanent.

- Standard Deduction – The standard deduction has been increased to $15,750 per person ($31,500 if married filing jointly). Additionally, a $6,000 deduction for individuals over 65 has been introduced, phasing out at incomes starting at $75,000 for individuals ($150,000 if married filing jointly).

- Above-the-Line Charitable Deductions – Starting January 1, 2026, individuals who take the standard deduction can claim a charitable deduction of up to $1,000 ($2,000 if married filing jointly).

- AGI Ceiling on Charitable Income Tax Deductions – The final bill permanently extends the 60% AGI limitation for cash gifts made to certain qualifying charities.

- AGI Floor on Charitable Income Tax Deductions – As of 2026, individuals who do itemize can deduct charitable donations to the extent they exceed 0.5% of their adjusted gross income. The disallowed portion may be eligible for carryforward to the following year. Corporations similarly can only deduct charitable donations to the extent they exceed 1% of their adjusted gross income.

- Limits on Itemized Deductions – The final bill creates a new limitation on all itemized deductions, including the deduction for state and local taxes (SALT), starting in 2026. Itemized deductions are reduced by 2/37 of the lesser of total itemized deductions or the amount of taxable income in excess of the 37% bracket threshold. Notably, this limitation does not apply to the qualified business income (QBI) deduction from pass-through entities.

- 529 Accounts – The annual limit for distributions for K-12 expenses has been increased from $10,000 to $20,000, and the bill also expands the types of expenses that qualify.

- Trump Accounts – Starting January 1, 2026, these accounts allow taxpayers to contribute up to $5,000 per year (indexed for inflation) to a tax-advantaged savings account for a child under age 18, essentially structured as non-Roth IRA accounts for minors. Funds cannot be accessed before age 18, and once distributions are taken, the rules applicable to IRAs will apply. There will be a “Pilot Program” allowing a $1,000 government-provided “baby bonus” for children born within the next four years.

Other Key Features Impacting Nonprofits and Other Tax-exempt Organizations:

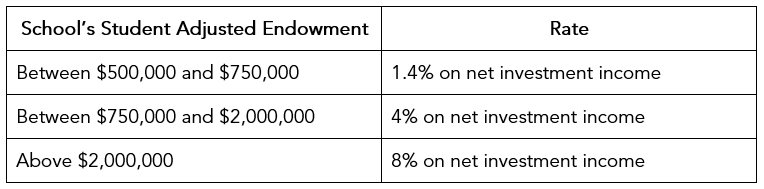

- College and University Endowment Tax – The final bill created a multi-tiered endowment tax rate structure based on each impacted school’s “student adjusted endowment,” which calculates the investment assets per student. The new tax rates are as follows:

The endowment tax impacts schools with at least 3,000 tuition-paying students, excluding smaller schools from the tax regardless of endowment size.

The final bill also includes new reporting requirements related to the endowment tax. Schools will be required to report the number of tuition-paying students on their annual returns.

Under the final bill, student loan interest and royalty income from intellectual property developed by students and faculty using federal funding are included in net investment income for purposes of calculating the tax. - Executive Compensation Excise Tax – The final bill expands the excise tax on compensation over $1 million paid by certain tax-exempt organizations, including private foundations and related entities, to include all current and former employees of the organizations, not just their top five most highly compensated current and former employees. The final bill limits former employees to those who were employed during tax years beginning after December 31, 2016

- Tax Credit for Gifts to Certain Scholarship Granting Organizations – The final bill creates a new tax credit (up to $1,700 per year, reduced by any state tax credit) for contributions to scholarship granting organizations (SGOs) – 501(c)(3) organizations that provide scholarships to students from kindergarten through college. Unlike a charitable contribution, this contribution would be a direct dollar-for-dollar reduction of the donor’s federal income tax liability, up to $1,700. The expectation is that these contributions will largely benefit private schools, both secular and religious, and is popular among school-choice advocates.

Key Features Impacting Businesses:

- Qualified Business Income Deduction: The bill makes permanent the 20% deduction for QBI (a/k/a the Section 199A deduction) that many owners of sole proprietorships, partnerships, S corporations and some trusts and estates may be eligible for.

- Expensing: There is a reinstatement as permanent of the 100% first-year “bonus depreciation” (that had phased out since 2022). Additionally, the cap on Section 179 deduction for qualified equipment and certain other assets was increased from $1 million to $2.5 million, with phase-out starting at $4 million.

- R&D: The legislation provides for immediate expensing of domestic R&D expenses (foreign R&D must still be amortized over 15 years), with potential “catch-up” amendment possible for capitalized R&D expenses on prior year returns filed for tax years after 2021.

- Qualified Small Business Stock: Three key changes to Section 1202 regarding QSBS benefits are implemented – (1) shortening the holding period to 3 years from 5 years, in which a 50% gain exclusion begins in year 3, 75% in year 4 and 100% after year 5, (2) increasing the capital gain exclusion to $15 million from $10 million, and (3) increasing the gross asset limit to $75 million from $50 million.

- 1099 Information Reporting: The bill increases the reporting threshold for payments to independent contractors and for miscellaneous income from $600 to $2,000, applicable to payments made after December 31, 2025. (Forms 1099-NEC and 1099-MISC)

Contact Us

For more information on how these changes impact your tax planning, please contact your Hemenway & Barnes advisor.