One, Big, Beautiful Bill: Estate Tax Changes

On May 22, 2025, the U.S. House of Representatives passed President Trump’s The One, Big, Beautiful Bill, which proposes extending the estate tax provisions of the Tax Cuts and Jobs Act (TCJA) beyond their current expiration date at the end of this year. While the bill is still under consideration in the Senate, the proposed extension appears to have growing support.

We are closely monitoring the bill, especially the tax and estate planning implications. We have highlighted some of the key features of the proposals here:

Potential Changes:

- Estate, Gift and GST Taxes – The House and Senate appear to agree on permanently increasing the exemption for estate, gift and GST taxes to $15 million per person ($30 million per married couple) starting in 2026, with indexing for inflation going forward.

- State and Local Taxes (SALT) – The House version made the cap on deductions for state and local taxes (the SALT cap) permanent and increased the SALT cap from $10,000 ($5,000 for a married taxpayer filing separately) to $40,000 for married couples with incomes up to $500,000. There is significant debate on the SALT cap. The Senate version also permanently extends the SALT cap but maintains the $10,000 limit. However, the Senate Finance summary notes this provision “is the subject of continuing negotiations.”

- Trump Accounts – The House version creates “Trump Accounts,” starting January 1, 2026. These accounts allows taxpayers to contribute up to $5,000 per year (indexed for inflation) to a tax-advantaged savings account for a child under age 8. Funds cannot be accessed before age 18. If funds are used for qualified purposes, such as higher education or buying a first home, the assets will be taxed as long-term capital gains. It also includes a $1,000 government-provided “baby bonus” for children born within the next four years. The Senate and House versions are very similar.

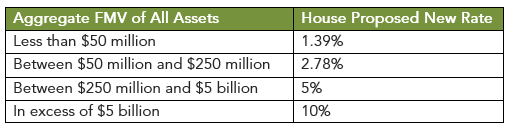

- Tax on University Endowments – The House version increases the tax on net investment income of private university endowments, with graduated rates based on the size of the endowed assets per student. The Senate version also increases the tax, but, at different rates and endowment sizes. The Senate version does not increase the tax as steeply.

- Tax on Private Foundations– The House version implements a graduated tax on the net investment income of private foundations. The Senate version leaves the tax on foundation net investment income static at 1.39%.

Congressional Republicans and President Trump have set a goal to pass the tax legislation by July 4, 2025.

Contact Us

For more information on tax or estate planning strategies, please contact a member of our Private Client Group, or the authors of this advisory.